Market Summary

In Q2 2024, capital market participants continued to sift through various economic indicators looking for any signal that the Federal Reserve (the “Fed”) would begin to cut interest rates. The market’s yearning for rate cuts began in earnest in Q4 2023 and has driven outperformance in pockets of the market, where companies may benefit from a lower discount rate and borrowing costs. With the market at one point pricing in upwards of seven rate cuts this year, the Fed funds rate remains at 5.25% – 5.50% following a series of rapid increases initiated in March 2022. The persistence of higher-for-longer inflation is the primary culprit for the lack of Fed action so far this year, as they cannot risk a reacceleration of inflation should they decide to cut rates too soon. While their stated inflation target is 2%, there still may be room for rate cuts if the long-term inflation rate settles around 3%, but not as much as more speculative investment vehicles, that benefitted to a greater degree from near zero-percent interest rates during the 2010’s, are hoping for, and pricing in.

The narrow breadth and leadership of large-cap indexes continue to signal caution. As of this writing, six stocks comprise 31% of the S&P 500 and have accounted for about 65% of the index’s total return this year. There are some striking similarities to the “tech bubble” that peaked in early 2000, where the top ten stocks in the S&P 500 accounted for 27% of the index. The lack of breadth today is even more extreme. Interestingly, we note that Cisco’s 5-year annualized return of 105% from March 31, 1995, through March 31, 2000, is astonishingly like that of Nvidia’s 5-year total annualized return of 98% through June 30, 2024. As the tech bubble started to deflate late in 2000, Cisco would go on to fall (87%) over the next 30 months. This ushered in a difficult decade for growth stocks, where from 2000 to 2010, large-cap domestic growth stocks fell (33%) while other investments like bonds, small-cap stocks, and emerging markets outperformed.

While we don’t necessarily foresee a similar “crash” in technology stocks forthcoming, we question the impact that items such as the advent of passive investing and more quantitative-based trading models have had on the narrow breadth and leadership we currently see. These tools have led to higher correlations and lower dispersion in stocks with higher market capitalizations as broad-based flows move into and out of those names daily for little fundamental reason related to the specific group of stocks. Many investors who partake in this investing style may have little idea of the concentration risk they are taking, especially given that the benefits of such styles are pitched as diversification and risk mitigation tools. When combined with historical Fed intervention over the last fifteen years, we are unsure if the long-term effects and reverberations have yet to be fully realized.

The S&P 500 gained 4.3% in Q2 and 15.3% in the year’s first half, driven primarily by technology and AI narratives. While there certainly will be some long-term AI winners, for the market to be pricing in every large-cap stock that mentions AI in their press release as an emphatic AI winner seems disingenuous. When combined with a lack of breadth in the major indexes and compounding factors over time that drive runaway momentum, such as passive and quant-based investing, the result is the market we see today, where large-cap stocks are rising at an unabated rate with no concern for price discovery.

While broad mid-and small-cap stocks faced overall losses, our small-cap value strategy has outperformed the Russell 2000 Value year-to-date by more than 9%. This highlights our bottom-up fundamental approach, which focuses on idiosyncratic, stock-specific catalysts backed by strong balance sheets and ample free cash flow. We continue to deploy our philosophy and process steadily across all market environments, as we have done since the 1990s.

Performance Highlights1

The Easterly Snow Small Cap Value strategy experienced a slightly negative performance of -2.23% in the second quarter of 2024, outperforming its benchmark, the Russell 2000 Value Index, by -3.64%. Selection and allocation effects positively drove the strategy’s relative performance.

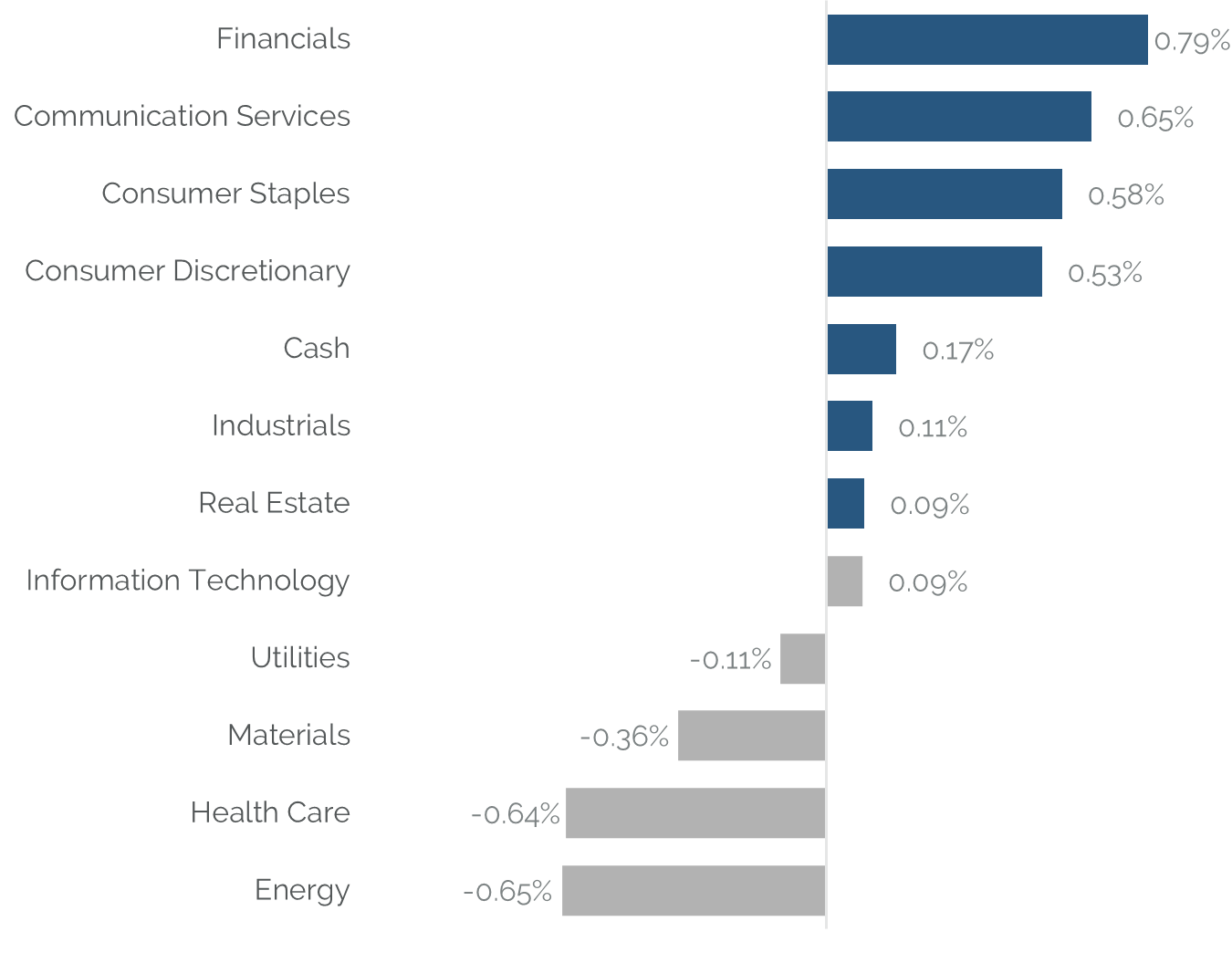

On a sector level, the Financials, Communication Services, and Consumer Staples sectors significantly contributed to the strategy’s outperformance due to strong stock selection within these sectors. Conversely, the Energy, Health Care, and Materials sectors detracted from the overall performance, primarily due to negative stock returns in these areas. Cash provided protection during this period of overall negative benchmark returns.

Performance Attribution2

Top 5 Performance Contributors

| Stock | Avg Weight % | Contribution % (net) |

|---|---|---|

| BRINKER INTERNATIONAL INC | 4.14 | 1.66 |

| CINEMARK HOLDINGS INC | 3.25 | 0.65 |

| JACKSON FINANCIAL INC-A | 4.38 | 0.57 |

| PILGRIM'S PRIDE CORP | 4 | 0.45 |

| ABM INDUSTRIES INC | 1.95 | 0.26 |

Brinker International (EAT)

Brinker International was the largest contributor to performance during the quarter, outperforming the Consumer Discretionary sector. Several key financial and operational successes drove this strong performance. The company reported an EPS of $1.24 on total revenue of $1.12 billion, reflecting solid revenue growth and effective cost management. Restaurant-level operating margin improved by 110 basis points quarter-over-quarter, driven by favorable food and beverage expenses, which improved by 170 basis points year-over-year, and labor expense management, which improved by 20 basis points. These results and effective marketing strategies, such as the 3-for-me advertising campaign, which saw an increase in higher-tier orders, highlight the company’s strong operational momentum.

Cinemark Holdings (CNK)

Cinemark Holdings (CNK) continued to perform well in the second quarter of 2024, significantly outperforming the broader Communication Services sector. This robust performance can be attributed to better-than-expected financial performance despite continued choppiness in box office results. CNK posted first-quarter revenue of $579 million, surpassing estimates by 3.8%, and an adjusted EBITDA of $70.7 million, exceeding projections by 28%. The company maintains market share gains, particularly in the U.S., where average ticket pricing and concession spending remain healthy.

Jackson Financial (JXN)

Jackson Financial delivered a strong performance in the second quarter of 2024, outpacing the broader Financials sector. Key drivers included an adjusted EPS of $4.23, surpassing street estimates of $3.75, and significant sales growth in registered index-linked annuities, which surged by 117% year-over-year to $1.2 billion. The company’s total annuity sales reached $3.7 billion, an 18% year-over-year increase.

Top 5 Performance Detractors

| Stock | Avg Weight % | Contribution % (net) |

|---|---|---|

| BLOOMIN' BRANDS INC | 3.13 | -1.19 |

| DELEK US HOLDINGS INC | 3.7 | -0.77 |

| PHOTRONICS INC | 3.81 | -0.51 |

| INTEGRA LIFESCIENCES HOLDING | 2.18 | -0.47 |

| ADVANCE AUTO PARTS INC | 1.6 | -0.45 |

Bloomin’ Brands (BLMN)

Bloomin’ Brands underperformed this past quarter as the company reported EPS of $0.70 on total revenue of $1.20 billion, both slightly below expectations. U.S. same-store sales were down 1.6%, with Outback Steakhouse reporting a 1.2% decline. Traffic dropped by 430 basis points, and restaurant-level operating margin fell to 16.0%, down 190 basis points year-over-year. Key events affecting performance included CEO David Deno’s retirement announcement and the exploration of strategic alternatives for the Brazil business, which contributed to investor uncertainty. These factors, along with increased labor costs and higher operational expenses, negatively impacted the stock’s performance

Delek US Holdings (DK)

Delek US Holdings (DK) underperformed in the first quarter of 2024, significantly trailing the Energy sector. Despite reporting an adjusted EBITDA of $159 million, which beat the consensus of $141 million, the company’s refining segment faced challenges. Refining adjusted EBITDA was $106 million, impacted by approximately $30 million due to weather issues in January at Big Spring and $10 million from planned maintenance at Krotz Springs. Additionally, despite healthy cash flow conversion and free cash flow (FCF) of $126 million, investor concerns over the delayed strategic process to unlock value contributed to the stock’s decline.

Photronics (PLAB)

Photronics underperformed in the first quarter of 2024. The company reported EPS of $0.46 on total revenue of $217 million, missing the guidance of $0.54 on $230 million. Operating margin dropped to 25.8%, down 80 basis points quarter-over-quarter and 340 basis points year-over-year due to increased R&D expenses and pricing power degradation. Notable challenges included the $3 million impact of the Taiwan earthquake and weaker-than-expected demand from China post-Chinese New Year.

Source: SEI Global Services as June 30, 2024

1Securities shown represent the largest contributors and detractors to the portfolio’s performance for the period and do not represent all holdings within the portfolio. There is no guarantee that such holdings are currently or will remain in the portfolio. For a complete list of holdings and an explanation of the methodology employed to determine this information, please contact Easterly. This information is not to be construed as an offer to buy or sell any financial instrument nor does it constitute an offer or invitation to invest in any fund managed by Easterly and has not been prepared in connection with any such offer.

2Performance shown is the Easterly Investment Partners LLC (“the Firm”) Snow Small Cap Value composite in USD. Past performance is not indicative of future results. Gross performance results do not include advisory fees and other expenses an investor may incur, which when deducted will reduce returns. Changes in exchange rates may have adverse effects. Net performance results reflect the application of a model investment management fee which is higher than the actual average weighted management fee charged to accounts in the composite applied to gross performance results. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. The Firm claims compliance with the GIPS® standards; this information is supplemental to the GIPS® report included in this material. Returns greater than one year are annualized

Trailing Performance

as of June 30, 2024

| QTD | YTD | 1 Yr | 3 Yr | 5 Yr | 7 Yr | 10 Yr | Since Inception* | |

|---|---|---|---|---|---|---|---|---|

| Composite (gross) | -2.17% | 8.83% | 20.03% | 7.48% | 15.12% | 11.69% | 7.70% | 9.77% |

| Composite (net) | -2.34% | 8.45% | 19.19% | 6.73% | 14.33% | 10.92% | 6.95% | 9.01% |

| Russell 2000 Value | -3.64% | -0.85% | 10.90% | -0.53% | 7.07% | 5.88% | 6.22% | 6.09% |

Calendar Year Performance

| 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Composite (gross) | 22.51% | -6.68% | 28.44% | 24.16% | 19.39% | -18.81% | 8.35% | 22.75% | -15.99% | 4.92% |

| Composite (net) | 21.66% | -7.33% | 27.56% | 23.31% | 18.57% | -19.39% | 7.60% | 21.91% | -16.59% | 4.19% |

| Russell 2000 Value | 14.65% | -14.48% | 28.27% | 4.63% | 22.39% | -12.86% | 7.84% | 31.74% | -7.47% | 4.22% |

Source: SEI Global Services

*Inception: 10/31/06

Performance shown is the Easterly Investment Partners LLC (“the Firm”) Snow Small Cap Value composite in USD. Past performance is not indicative of future results. Gross performance results do not include advisory fees and other expenses an investor may incur, which when deducted will reduce returns. Changes in exchange rates may have adverse effects. Net performance results reflect the application of a model investment management fee which is higher than the actual average weighted management fee charged to accounts in the composite applied to gross performance results. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. The Firm claims compliance with the GIPS® standards; this information is supplemental to the GIPS® report included in this material. Returns greater than one year are annualized.

Top 10 Holdings

| JACKSON FINANCIAL INC-A | 4.13% |

| PILGRIM'S PRIDE CORP | 4.06% |

| LINCOLN NATIONAL CORP | 3.95% |

| SILICON MOTION TECHNOL-ADR | 3.91% |

| BRINKER INTERNATIONAL INC | 3.89% |

| CINEMARK HOLDINGS INC | 3.65% |

| CNO FINANCIAL GROUP INC | 3.65% |

| PHOTRONICS INC | 3.60% |

| OLD NATIONAL BANCORP | 3.35% |

| DELEK US HOLDINGS INC | 3.29% |

| Total | 37.48% |

Excludes cash and cash equivalents.

References to securities, transactions or holdings should not be considered a recommendation to purchase or sell a particular security and there is no assurance that, as of the date of publication, the securities remain in the portfolio. Additionally, it is noted that the securities or transactions referenced do not represent all of the securities purchased, sold or recommended during the period referenced and there is no guarantee as to the future profitability of the securities identified and discussed herein. Top ten holdings information shown combines share listings from the same issuer, and related depositary receipts, into a singular holding to accurately present aggregate economic interest in the referenced company.

Attribution vs Russell 2000 Value

Source: Bloomberg

Holdings, sector weightings, market capitalization and portfolio characteristics are subject to change at any time and are based on a representative portfolio, and may differ, sometimes significantly, from individual client portfolios.

Outlook

As active managers, we look forward to environments like this, where correlations are elevated, and stocks trade in step. This enables us to identify price dislocations and populate our strategy with great companies whose stock price doesn’t reflect their underlying fundamental valuation. This helps us drive positive returns over full cycles, not just on a day-to-day or quarter-to-quarter cadence.

The valuation gap between large-cap and small-cap stocks remains at historically elevated levels. The Russell 2000 Value trades at 12x forward earnings, and the Easterly Snow Small Cap Value strategy at 9x forward earnings, relative to the S&P 500 at 21x, a 16% premium to its 10-year average.

The market continues to remain focused on the timing and magnitude of interest rate cuts from the Fed, which is looking more likely in the second half of the year even as they continue to reduce their own balance sheet (which stands in contrast to their balance sheet expansion during the 2010s, artificially suppressing yields). While certain pockets of the small-cap market may outperform (stocks with negative earnings and/or high debt levels) as rate cuts are initially priced in, we question how sustainable that outperformance may remain as the market prices in a normalized Fed Funds rate that may be higher than what those more speculative pockets of the market are hoping for.

As we work through a U.S. Presidential election cycle likely to bring volatility, items we’re paying heightened attention to include the U.S. jobs market, where unemployment has increased above 4%. The jobs market has shown impressive resilience, while other cracks in the U.S. economy have emerged over the last few quarters. Consumer spending, which is 70% of GDP, is declining as credit card balances continue to rise. Retail sales are slowing and, when factoring in inflation, have, in fact, turned negative. $1T in corporate debt annually continues to roll into issuances with much higher costs. We are unsure how this will impact more leveraged corporations, especially if cash flow falters. A housing market that looks increasingly unaffordable for many, especially younger people without familial financial assistance, may reshape how that younger cohort allocates their discretionary income. We are keeping a steady eye on the US fiscal deficit, the associated debt servicing costs, and the ramifications of legislators’ inability to rein in spending.

The Easterly Snow investment team’s core competency is to invest the same stylistically through all of this market noise. We remain focused on allocating capital to companies going through short-term difficulties with great balance sheets, material free cash flow, and a path to earnings recovery resulting in asymmetric upside/downside return profiles.

GIPS® Report

Easterly Investment Partners LLC Snow Snow Small Cap Value Composite

Composite Inception Date: October 31, 2006

Composite Creation Date: 07/01/2021

| Year End | Composite Performance | Annualized 3-Year Standard Deviation | Total Assets (millions) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Gross | Net | Russell 2000 Value | Composite | Russell 2000 Value | Composite Dispersion | Total Firm Assets | Firm (AUM) | Firm (AUA)* | Composite | Number of Accounts | |

| 2023 | 22.51% | 21.66% | 14.65% | 24.00% | 22.06% | N/A | 1,730 | 1,090 | 640 | 64 | Five or fewer |

| 2022 | -6.68% | -7.33% | -14.48% | 33.38% | 27.66% | N/A | 1,834 | 1,341 | 493 | 55 | Five or fewer |

| 2021 | 28.44% | 27.56% | 28.27% | 32.10% | 25.35% | N/A | 2718 | 1540 | 1178 | 77 | Five or fewer |

| 2020 | 24.16% | 23.31% | 4.63% | 32.68% | 26.12% | 0.10% | - | - | 78 | Five or fewer | |

| 2019 | 19.39% | 18.57% | 22.39% | 20.50% | 15.70% | 0.20% | - | - | 82 | Five or fewer | |

| 2018 | -18.81% | -19.39% | -12.86% | 20.10% | 15.80% | N/A | - | - | 103 | Five or fewer | |

| 2017 | 8.35% | 7.60% | 7.84% | 18.20% | 14.00% | N/A | - | - | 421 | 6 | |

| 2016 | 22.75% | 21.91% | 31.74% | 18.40% | 15.50% | 0.60% | - | - | 627 | 10 | |

| 2015 | -15.99% | -16.59% | -7.47% | 15.00% | 13.50% | 0.50% | - | - | 643 | 12 | |

| 2014 | 4.92% | 4.19% | 4.22% | 15.20% | 12.80% | N/A | - | - | 557 | 9 | |

*Firm-wide advisory- only assets. Assets under Advisement (AUA) includes the assets where Easterly Investment Partners (“Easterly”) provides its advisory services in similar strategies and does not have discretionary trading authority.

Firm Definition

For purposes of complying with the GIPS® standards, the firm is defined as Easterly Investment Partners LLC (“EIP”) which is an SEC registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, effective January 2019. The firm was redefined on 1/1/2023 to reflect that EIP is comprised of two distinct firms: the institutional asset management operations, investment strategies, performance track records, certain employees and client accounts of Levin Capital Strategies, which were acquired by EIP in March 2019, and Snow Capital Management LLC’s (“SCM”) asset management business, investment strategies, performance track records, client accounts, and certain employees, acquired by EIP in July 2021.

Firm Verification Statement

Easterly claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Easterly has been independently verified for the period April 1, 2019 through December 31, 2023. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis.

Composite Verification Statement

The Small Cap Value Composite has had a performance examination from composite inception date through December 31, 2023. The verification and performance examination reports are available upon request.

Composite Description

The Small Cap composite provides exposure to long-only US publicly-listed securities and ADRs, and may occasionally invest in convertible and corporate bonds, taking into account various factors. The strategy is biased toward Small capitalization value stocks, and position sizes range between 0.5% to 5%, with liquidity as a consideration.

Benchmark Description

The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. Indexes are unmanaged. It is not possible to invest directly in an index.

Performance Calculation

All returns are calculated and presented in US dollars based on fully discretionary AUM, including those investors no longer with the firm. All gross composite returns are net of transaction costs and foreign withholding taxes, if any, and reflect the reinvestment of interest income and other earnings. Net performance results reflect the application of a model investment management fee which is higher than the actual average weighted management fee charged to accounts in the composite applied to gross performance results. Composite net returns are calculated by reducing daily gross returns by an amount where the monthly net return will be the monthly gross return reduced by 1/12th of the highest advisory fee rate. Monthly net returns are then geometrically linked to calculate the annual net return. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. Actual investment advisory fees incurred by clients will vary. Policies for valuing investments, calculating performance, and preparing GIPS reports are available upon request. A list of composite descriptions and a list of broad distribution pooled funds are available upon request. Past performance is not indicative of future performance. Results may be higher or lower based on IPO eligibility, and actual investor’s returns may differ, depending upon date(s) of investment(s). Additional information is available upon request. The Small Cap Value Composite has removes accounts from the composite for the period of significant cash flow of greater than or equal to $20 million.

Investment Management Fee Schedule

The current standard management fee schedule for a segregated account managed to the composite strategy is as follows: 0.70% on the first $25 million; 0.55% on the next $75 million; 0.50% on the next $100 million; 0.45% on the next $100 million; 0.35% on the balance.

Composite Dispersion

The annual composite dispersion, if shown, is an asset-weighted standard deviation calculated using gross returns for the accounts in the composite the entire year. The internal dispersion measure is not applicable if there are five or fewer portfolios in the composite for the entire year if that is the reason this is N/A.

Standard Deviation

The annualized 3-year standard deviation represents the annualized standard deviation of actual gross composite and benchmark returns, using the rolling 36 months ended each year end. Standard deviation is a measurement of historical volatility of investment returns.

Trademark

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

Important Disclosures

© 2024. Easterly Asset Management. All rights reserved.

Easterly Asset Management’s advisory affiliates (collectively, “EAM” or “the Firm”), including Easterly Investment Partners LLC, Easterly Funds LLC, and Easterly EAB Risk Solutions LLC (“Easterly EAB”) are registered with the SEC as investment advisers under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about the firm, including its investment strategies and objectives, can be found in each affiliate’s Form ADV Part 2 which is available on the www.sec.gov website. This information has been prepared solely for the use of the intended recipients; it may not be reproduced or disseminated, in whole or in part, without the prior written consent of EAM.

No funds or investment services described herein are offered or will be sold in any jurisdiction in which such an offer or sale would be unlawful under the laws of such jurisdiction. No such fund or service is offered or will be sold in any jurisdiction in which registration, licensing, qualification, filing or notification would be required unless such registration, license, qualification, filing, or notification has been affected.

The material contains information regarding the investment approach described herein and is not a complete description of the investment objectives, risks, policies, guidelines or portfolio management and research that supports this investment approach. Any decision to engage the Firm should be based upon a review of the terms of the prospectus, offering documents or investment management agreement, as applicable, and the specific investment objectives, policies and guidelines that apply under the terms of such agreement. There is no guarantee investment objectives will be met. The investment process may change over time. The characteristics set forth are intended as a general illustration of some of the criteria the strategy team considers in selecting securities for client portfolios. Client portfolios are managed according to mutually agreed upon investment guidelines. No investment strategy or risk management techniques can guarantee returns or eliminate risk in any market environment. All information in this communication has been obtained from sources believed to be reliable but cannot be guaranteed. Investment products are not FDIC insured and may lose value.

Investments are subject to market risk, including the loss of principal. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate. The information contained herein does not consider any investor’s investment objectives, particular needs, or financial situation and the investment strategies described may not be suitable for all investors. Individual investment decisions should be discussed with a personal financial advisor.

Any opinions, projections and estimates constitute the judgment of the portfolio managers as of the date of this material, may not align with the Firm’s opinion or trading strategies, and may differ from other research analysts’ opinions and investment outlook. The information herein is subject to change without notice and may be superseded by subsequent market events or for other reasons. EAM assumes no obligation to update the information herein.

References to securities, transactions or holdings should not be considered a recommendation to purchase or sell a particular security and there is no assurance that, as of the date of publication, the securities remain in the portfolio. Additionally, it is noted that the securities or transactions referenced do not represent all of the securities purchased, sold or recommended during the period referenced and there is no guarantee as to the future profitability of the securities identified and discussed herein. As a reminder, investment return and principal value will fluctuate.

The indices cited are, generally, widely accepted benchmarks for investment performance within their relevant regions, sectors or asset classes, and represent non managed investment portfolio. It is not possible to invest directly in an index.

This communication may contain forward-looking statements, which reflect the views of EAM and/or its affiliates. These forward-looking statements can be identified by reference to words such as “believe”, “expect”, “potential”, “continue”, “may”, “will”, “should”, “seek”, “approximately”, “predict”, “intend”, “plan”, “estimate”, “anticipate” or other comparable words. These forward-looking statements or other predications or assumptions are subject to various risks, uncertainties, and assumptions. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. Should any assumptions underlying the forward-looking statements contained herein prove to be incorrect, the actual outcome or results may differ materially from outcomes or results projected in these statements. EAM does not undertake any obligation to update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by applicable law or regulation.

Past performance is no guarantee of future results.

20240731-3752786