Executive Summary

At the risk of disappointing our more quantitatively oriented readership, this is a deliberately math-light discussion of a mathematically grounded problem. Our investment team views that as a feature, not a bug.

Modern Portfolio Theory (MPT), through the work of Harry Markowitz and Bill Sharpe, provides a sound framework for constructing portfolios using return, risk, and covariance. We will not define MPT in this work but rather acknowledge that its core principles continue to guide many of the portfolio construction decisions used by individuals and institutions today.

While asset allocation frameworks have come under increasing scrutiny over the past decade, I believe a different perspective may add value to the discussion. In my view, many of the challenges investors encounter have less to do with the mathematics of diversification1 and more to do with how these principles are applied in practice.

This discussion challenges a widely accepted assumption: that capitalization-weighted indices are not only efficient in cost, but also efficient in construction. While this is not a completely new observation, the distinction between those two ideas has become conflated. Low-cost exposure has increasingly become a substitute for thoughtful portfolio construction, reinforced by an extended period of accommodative monetary policy, abundant liquidity, and relatively stable correlation structures across asset classes.

Cap-weighted indices are designed to provide efficient access to market beta. They are not specifically designed to optimize diversification, manage concentration, or account for how correlations behave under stress. More importantly, if the underlying equity exposure used as a portfolio building block is not constructed with diversification in mind, then the efficient frontier derived from those inputs may become less efficient in practice. Portfolio optimization may be directionally sound in theory, but potentially suboptimal in practice if the underlying inputs are increasingly concentrated or highly correlated from the outset.

This distinction has become more relevant as index-based exposure has come to dominate equity allocation. Increasingly, investors begin portfolio construction from similar underlying exposures, reducing the potential for true diversification before any asset allocation decisions are made. At the same time, fixed income has not always provided the diversification benefits many portfolios historically relied upon.

The issue is not whether diversification works. The issue is whether the way portfolios are currently constructed is consistently delivering the diversification investors expect.

From Theory to Implementation

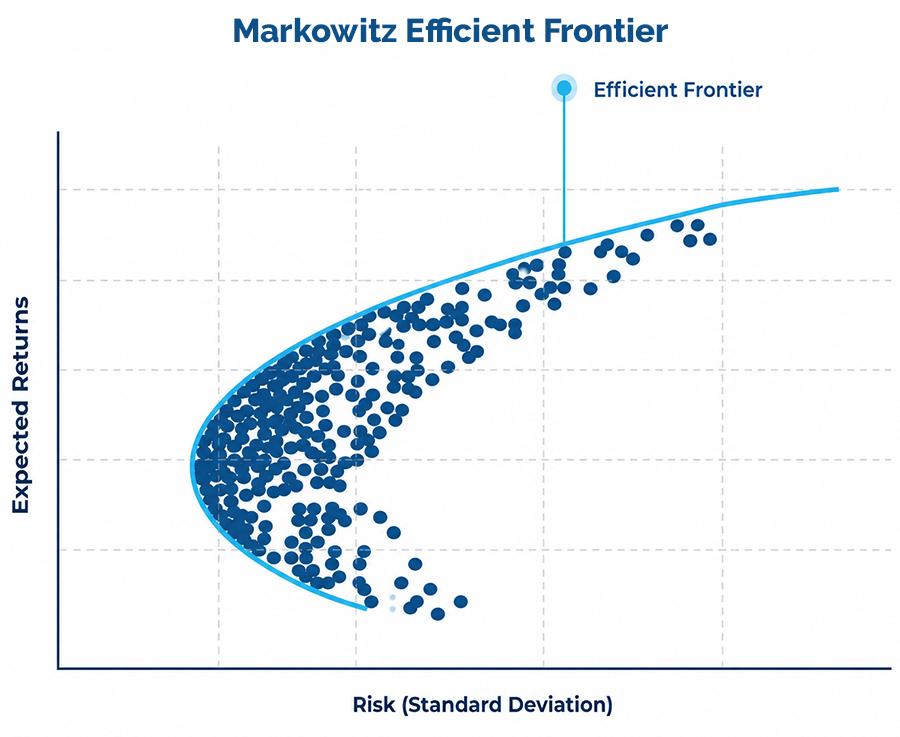

Markowitz established that portfolios should be built to optimize return relative to risk, where risk includes how assets move relative to one another (Figure 1).

Figure 1

Source: Markowitz, Harry. “Portfolio Selection.” Journal of Finance, 1952.

Sharpe extended that framework by distinguishing between systematic risk, for which investors may be compensated, and idiosyncratic risk, which MPT assumes can largely be diversified away.

From there emerged the concept of the “market portfolio,” the theoretically optimal risky portfolio under a set of simplifying assumptions, including broad diversification and relatively stable correlations among assets.

Jack Bogle, founder of Vanguard and widely regarded as a pioneer of passive investing, translated that framework into practical implications: own the market, minimize cost, and stay invested. That insight improved outcomes for a generation of investors. However, it rests on an important assumption: that the index investors own remains a sufficiently diversified proxy for the theoretical market portfolio. We believe that assumption deserves renewed examination.

Exposure Is Not Construction

Passive investing has been effective in reducing costs and helping investors avoid many of the behavioral mistakes that often undermine long-term investment outcomes. Those benefits should not be dismissed. But low-cost exposure is not the same as optimal portfolio construction. That distinction matters. In that sense, the question may not be whether asset allocation has failed, but whether the building blocks used within those allocations were ever designed to deliver the diversification many investors expect.

Low-cost exposure is not the same as optimal portfolio construction.”

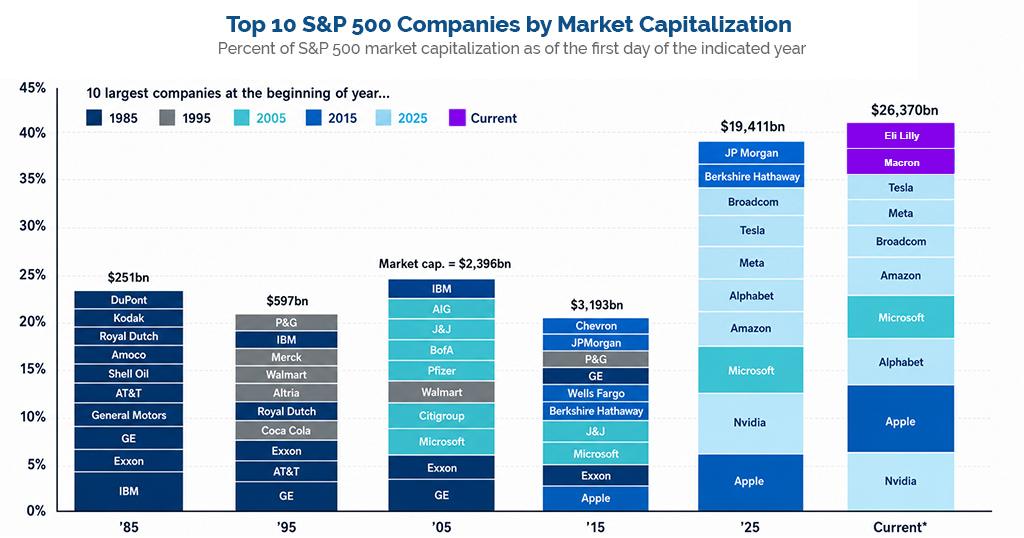

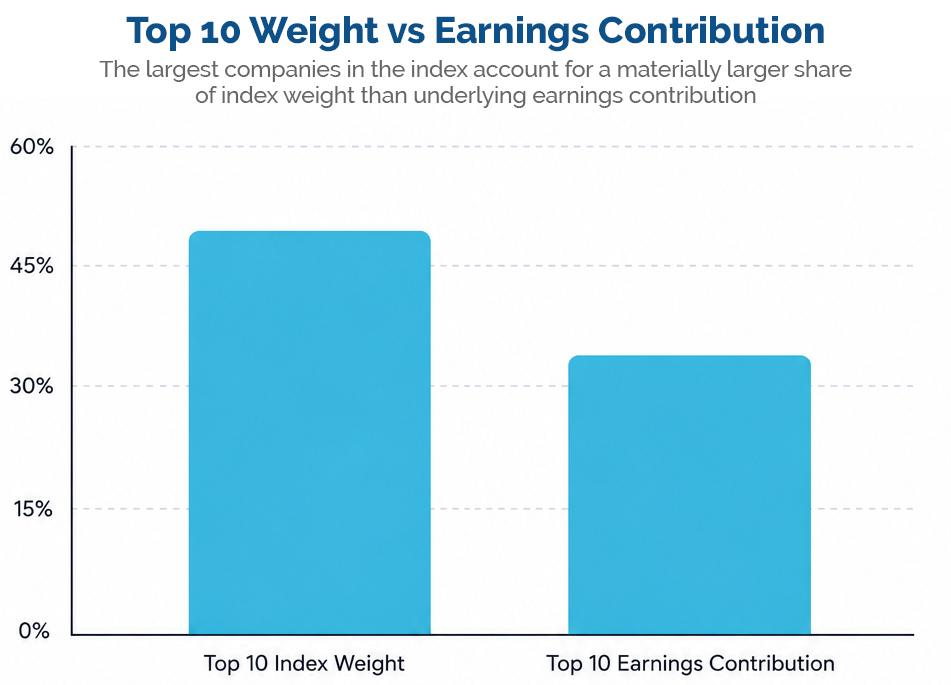

A capitalization-weighted index does not balance risk or optimize covariance. In practice, it reflects market capitalization and investor sentiment at a point in time. Over time, that means increasing exposure to what has already worked. That mechanism is not inherently flawed, but it does mean the portfolio weights evolve based on price, rather than diversification objectives (Figures 2, 3).

Figure 2

As of 5/29/2026. Source: J.P. Morgan Asset Management, Guide to the Markets, Q2 2026. https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

Figure 3

Source: RBC Wealth Management, The Great Narrowing: S&P Concentration” (2026). As of 1/22/2026 https://www.rbcwealthmanagement.com/en-us/insights/the-great-narrowing-sp-500-concentration

There is a deeper implication. If the underlying equity exposure used as a building block is not constructed with diversification in mind, then the efficient frontier derived from those inputs may be inherently distorted. Portfolio optimization may be directionally sound in theory, but potentially suboptimal in practice if the underlying inputs themselves are increasingly concentrated or highly correlated.

A manifestation of this dynamic is the growing tendency of the S&P 500 Index to perform very similarly to the NASDAQ. It is practically shown by how large a performance margin can be seen in market cap weighted indices versus their average cap versions.

As index-based exposure increasingly dominates equity allocation, portfolios may begin from a more uniform and correlated base than assumed. This raises the question of whether diversification is being reduced at the input level, before any asset allocation decisions are made. Over a full cycle, that distinction matters.

This raises the question of whether diversification is being reduced at the input level, before any asset allocation decisions are made.”

Concentration and Diversification

Recent market structure has made concentration hard to ignore. A relatively small number of companies have driven a significant share of index returns. An index can hold hundreds of names and still behave like a considerably narrower exposure beneath the surface. Diversification, in the Markowitz sense, is not about the number of positions held. It is about how those positions interact.

An index can hold hundreds of names and still behave like a considerably narrower exposure beneath the surface.”

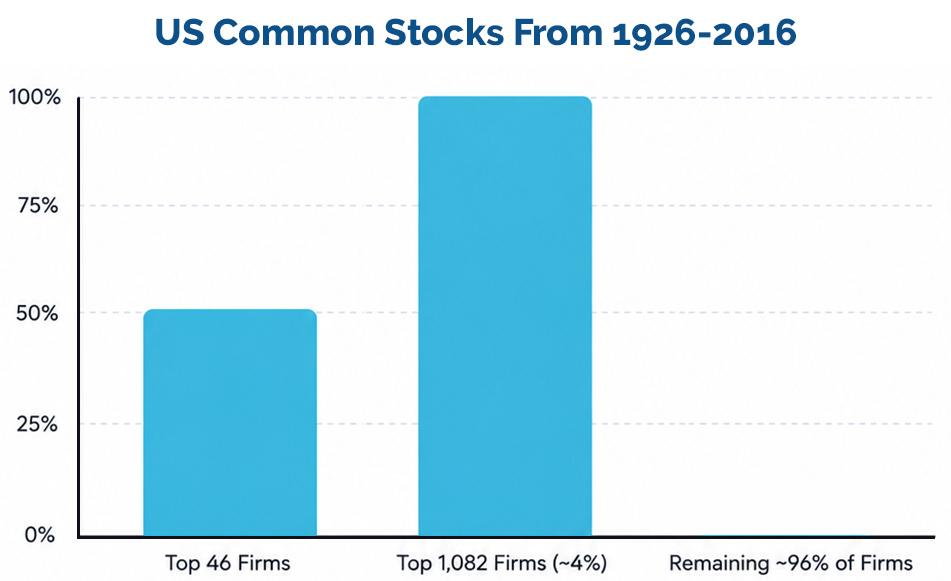

Hendrik Bessembinder, a finance professor whose research focuses on long-term equity returns and wealth creation, highlights an important paradox. Broad index exposure may increase the probability of owning the relatively small number of firms responsible for a disproportionate share of long-term wealth creation, while simultaneously creating portfolios that become increasingly dependent on a narrow subset of outcomes (Figure 4).

Figure 4

Source: Hendrik Bessembinder, “Do Stocks Outperform Treasury Bills?” Journal of Financial Economics, 2018. Analysis of U.S. common stocks, 1926-2016.

In practice, this also means that sector weights within capitalization-weighted indices increasingly reflect market expectations for future growth and profitability rather than current economic representation. As a result, indices can become progressively tilted toward sectors and companies associated with the strongest forward-looking narratives, further increasing concentration and expectation risk within the portfolio itself.

As weights concentrate and exposures increasingly align, diversification benefits may diminish. This dynamic often becomes most visible when conditions are less forgiving. While there continues to be debate surrounding the role of ETFs and passive flows in amplifying these effects, the more fundamental issue is that index construction itself already embeds many of these tendencies.

When Index Strength Masks Diversification Risk

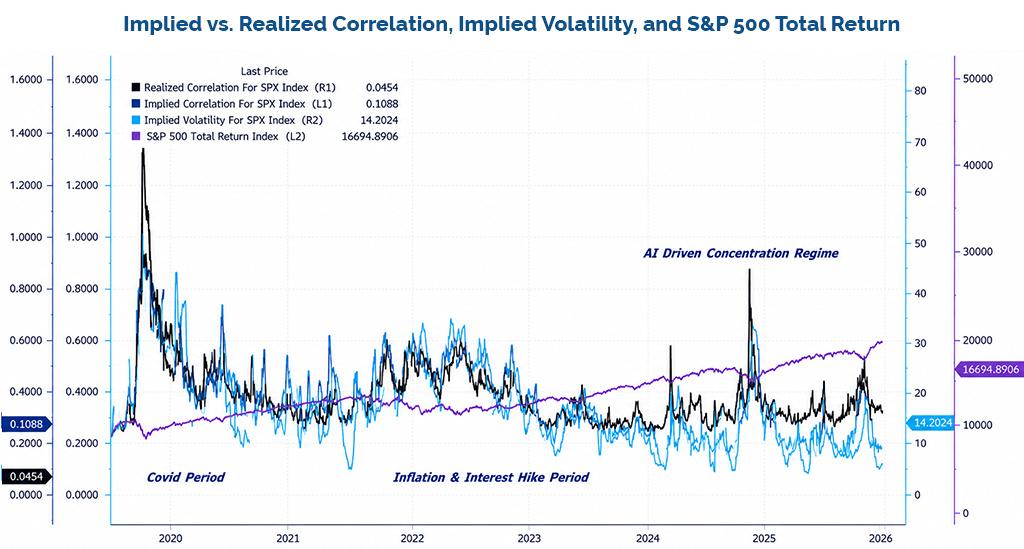

Over the last five years, investors have experienced several distinct market environments, including the COVID shock, the inflation and interest-rate tightening cycle, regional banking stress, and more recently, an AI-driven concentration rally led by a relatively narrow group of mega-cap stocks.

While headline indices ultimately advanced through much of this period, the underlying market experience was at times less stable than index-level returns alone might suggest (Figure 5a).

Figure 5a

Source: Bloomberg. Weekly observations from November 2016 through May 2026. As of 5/26/2026

Implied volatility, realized correlation, and implied correlation periodically diverged from one another, suggesting that traditional measures of market calm may not always fully reflect underlying diversification dynamics.

This distinction matters because many portfolios today begin with assumptions around diversification that may behave differently across market environments than some investors expect.

Passive flows, benchmark concentration, and increasingly crowded positioning may contribute to environments in which portfolios appear diversified by holdings count while behaving more similarly during periods of stress or rapid repricing. Recent market environments have demonstrated that strong index performance and narrowing market leadership can coexist alongside elevated concentration and changing correlation behavior beneath the surface.

In our view, this evolving market structure may warrant greater consideration of portfolio construction, correlation risk, and the role of adaptive risk management within modern equity portfolios.

As benchmark concentration and passive positioning continue to grow, portfolios may carry greater embedded correlation risk than holdings-based diversification metrics alone may suggest, particularly during periods of market stress or rapid repricing.

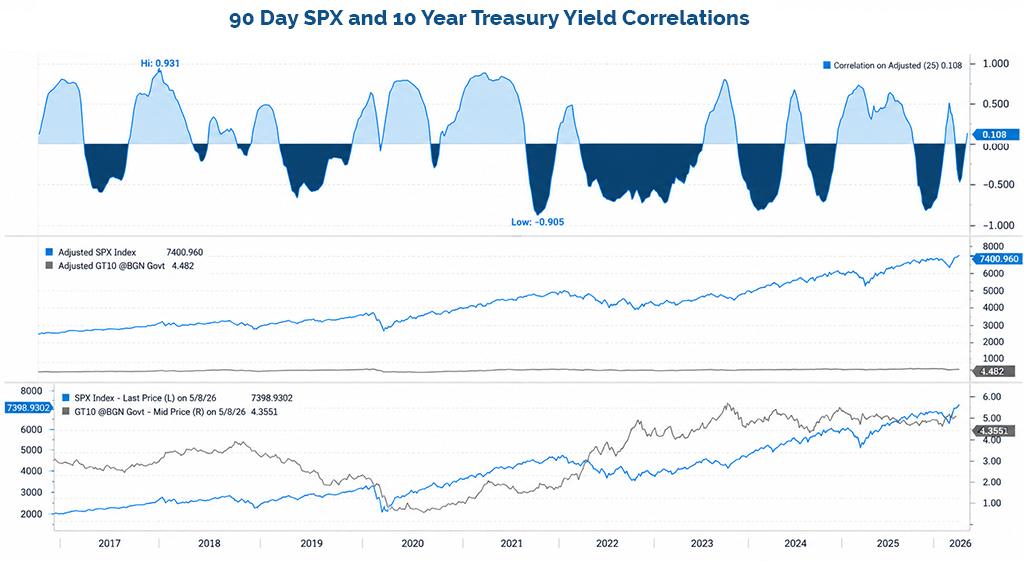

Correlation Is Not Stable

Diversification depends on imperfect correlations. That principal remains foundational to MPT and its many extensions. In practice, however, correlations are not stable. Historically, correlations have often risen during periods of market stress. Assets that appear diversified in stable environments can begin moving similarly during periods of volatility, uncertainty, or repricing. Equity portfolios expected to behave as broad collections of exposure can begin functioning more like a single exposure to market beta.

Diversification depends on imperfect correlations”

Fixed income, long relied upon as a stabilizing force within diversified portfolios, has not always provided the diversification benefits investors have historically expected, particularly during inflationary or rising-rate environments.

That experience reinforces a broader point: historical correlation relationships can and do change. When they do, diversification may become less effective precisely when investors expect them most (Figure 5b).

Figure 5b

Source: Bloomberg. Weekly data from 11/13/2016-5/13/2026.

Accordingly, investors should increasingly think about portfolios less through static asset allocation labels such as 60/40 or 60/20/20 and more through the lens of underlying risk exposures, correlation behavior, and portfolio function.

Traditional portfolio models were built during a period in which market regimes generally supported more stable correlation assumptions and liquidity conditions broadly supported passive asset appreciation. That environment allowed portfolios to rely heavily on static diversification assumptions and a favorable fixed income environment that may not always persist.

If correlation relationships become less reliable, the fundamentals of portfolio construction become even more important.

Behavior and Path of Returns

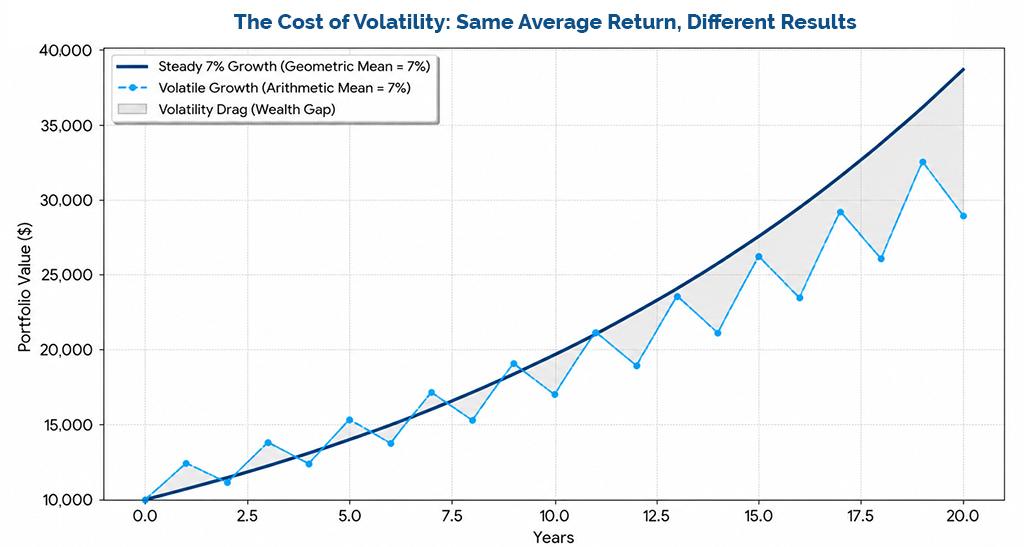

Investor outcomes may be influenced not only by long-term average returns, but also by the path taken to achieve them.

Large drawdowns and periods of elevated volatility can affect both portfolio values. They can influence investor behavior during periods of market stress, often at precisely the wrong moments (Figures 6, 7).

Figure 6

| Investment loss | Return needed to breakeven |

|---|---|

| -5% | +5.3% |

| -10% | +11% |

| -20% | +25% |

| -30% | +43% |

| -40% | +67% |

| -50% | +100% |

| -60% | +150% |

| -70% | +233% |

Source: Easterly Investment Partners. For illustrative purposes only and does not represent a forecast or guarantee of future performance. Calculations are based on simple mathematical relationships between percentage losses and the gains required to recover to a prior value.

Figure 7

Source: Easterly EAB. This chart illustrates how volatility drag impacts long-term outcomes. Even with the same 7% average return, the more volatile path results in lower ending wealth due to compounding effects. For illustrative purpose only.

As a result, some portfolio construction approaches seek to manage volatility and drawdown exposure in an effort to improve the consistency of the investment experience over time. The practical challenge is not simply whether a portfolio eventually recovers. It is whether investors remain invested long enough to participate in that recovery.

If portfolio structure amplifies drawdowns, the likelihood of emotionally driven investment decisions may also increase. This is one reason why the path of returns matters. The objective is not to eliminate risk. It is to improve how risk is experienced over time.

That distinction can have meaningful implications for both portfolio outcomes and investor behavior.

Benchmarking and the Cost of Missing Leadership

It is also worth considering whether modern index construction increasingly reflects a form of institutional regret minimization rather than diversification optimization.

For many investors, advisors, and professional allocators, the risk of materially underperforming the market’s largest winners may carry greater behavioral or career-related consequences than accepting elevated concentration risk. In that sense, capitalization weighting may function not only as a diversification framework, but also as a mechanism for minimizing the regret associated with missing leadership.

Over time, this dynamic can reinforce concentration and momentum within the market portfolio itself. This observation is not intended as a criticism of indexing. Rather, it highlights the practical realities of how capital is allocated and benchmarked. Investors are often evaluated relative to market outcomes, not necessarily relative to diversification efficiency.

As a result, concentration can become an accepted byproduct of benchmark adherence. Viewed through that lens, some of today’s concentration may be less a market anomaly and more a predictable outcome of the incentives embedded within modern portfolio management.

A Note on Regime

A prolonged period of declining interest rates and highly responsive monetary policy influenced both the depth and duration of market drawdowns.

Recoveries have often proved faster and more consistent than in many prior regimes. For investors, that experience reinforced the perception that broad market exposure alone was sufficient and that diversification challenges would ultimately resolve themselves through time and liquidity. It also reduced the perceived need for explicit risk management.

If policy flexibility is more constrained going forward, correlations may remain elevated for longer periods, drawdowns may persist, and volatility may become more a structural feature of markets rather than a temporary disruption. A shift in regime does not create these issues. It reveals them.

The question is not whether markets have permanently changed. The question is whether portfolios built under one set of assumptions remain as effective under another.

The Constraints of Active Management

The discussion thus far should not be interpreted as a simple active-versus-passive debate.

Many active managers operate under constraints that limit their ability to materially alter portfolio construction. Tracking error limits, benchmark awareness, liquidity requirements, and client expectations all influence investment decisions.

As a result, both active and passive portfolios often remain exposed to many of the same concentration and correlation dynamics. The principal sources of risk often remain surprisingly similar.

Both active and passive portfolios often remain exposed to many of the same concentration and correlation dynamics.”

The debate then becomes one of relative performance rather than structural efficiency. That distinction is important. If the objective is portfolio optimization in the Markowitz sense, then understanding the concentration and correlation characteristics of the underlying building blocks matters regardless of whether a manager is active or passive.

Too often, discussions focus on performance outcomes while giving less attention to the structural characteristics of the portfolio itself.

Implications for Portfolio Construction

If diversification is defined by how assets behave rather than simply how many assets are held, then portfolios built primarily on capitalization-weighted indices may carry more concentrated risk than investors intend. The issue may not be whether portfolios are properly diversified, but whether the inputs used to construct them were ever truly diversified to begin with.

For advisors and allocators, this raises several important considerations:

- Are equity allocations overly reliant on a single source of beta? Or conversely, on too wide a number of actually correlated positions or funds?

- How does the portfolio behave during periods of rising correlation?

- Are structural constraints limiting true diversification?

- Is drawdown potential risk aligned with client tolerance, or simply accepted?

These are not questions of market timing, but of portfolio design.

A Note on Portfolio Construction vs. Exposure

It is worth noting that some of the most successful long-term investors have not constructed portfolios by allocating across pre-packaged market exposures, but by assembling collections of differentiated and often idiosyncratic assets.

Several examples come to mind. Interestingly, many of these investors are respected precisely because they were willing to tolerate significant tracking error in pursuit of differentiated return streams and risk exposures.

What some of these investors sought was not simply diversification by holdings count, but diversification by underlying economic driver. In that sense, diversification is achieved through the sources of return themselves rather than through the weighting structure of an index.

Viewed through that lens, the approach arguably aligns more closely with the original Sharpe-Markowitz framework than portfolios whose diversification is largely determined by market capitalization and investor sentiment.

This is not an argument that every investor should attempt to replicate such approaches. It is simply a reminder that diversification can be pursued through multiple paths, and that exposure alone is not always synonymous with diversification.

Implementation Framework

If capitalization-weighted indices do not fully address concentration, correlation, and the path of returns, the solution is not to abandon them. They remain valuable tools and are unlikely to disappear from portfolio construction. Rather, the challenge is determining how best to complement them.

Several considerations may help improve portfolio resilience:

- Begin the asset allocation process with explicit volatility and drawdown risk objectives, then seek return targets that align with those constraints.

- Separate beta from risk management. Market participation and volatility management can be viewed as distinct portfolio objectives.

- Emphasize meaningful diversification within equities, managers, and style exposures rather than relying solely on asset-class labels.

- Focus on the path of returns, not simply long-term outcomes, particularly where sequence-of-return risk and investor behavior may influence results.

These principles do not eliminate risk. Rather, they seek to create a more intentional framework for managing it.

What This Looks Like in Practice

Improving diversification does not require abandoning market exposure. It requires rethinking how that exposure is delivered.

Potential approaches may include:

- Maintaining equity participation while seeking to manage downside risk through complementary portfolio structures.

- Utilizing shorter-dated instruments that can be adjusted more frequently as market conditions evolve.

- Reducing reliance on static correlation assumptions and incorporating exposures designed to behave differently across market environments.

- Building portfolios with greater awareness of concentration risk, drawdown sensitivity, and correlation behavior during periods of stress.

The objective is not to eliminate risk, but to reshape how it is experienced.

Conclusion

Bogle’s framework solved an important problem. It reduced costs, improved access, and helped many investors achieve better long-term outcomes. But it also relied on the assumption that the index itself provided sufficient diversification.

If we take Markowitz and Sharpe seriously, portfolio construction should not stop at exposure. If the building blocks themselves are not fundamentally constructed with diversification in mind, the resulting portfolio may be impacted by concentration and correlation dynamics that are often overlooked. The math is not the challenge. The application may be.

The math is not the challenge. The application may be.”

Passive investing may have solved for cost. It did not necessarily solve how portfolios behave across varying market environments or how investors experience those outcomes over time. If portfolio construction stops at exposure alone, diversification risks becoming more of an assumption than an intentional design choice.

Modern Portfolio Theory remains intellectually sound. The question is whether today’s implementation fully reflects its original intent. That distinction may matter more than investors realize.

References

Markowitz, H. Portfolio Selection (1952)

https://www.researchgate.net/publication/228051028_Portfolio_Selection

Sharpe, W. Capital Asset Pricing Model (1964)

https://finance.martinsewell.com/capm/Sharpe1964.pdf

Sharpe, W. Arithmetic of Active Management

https://web.stanford.edu/~wfsharpe/art/active/active.htm

Fama & French CAPM Overview

https://mba.tuck.dartmouth.edu/bespeneckbo/default/AFA611-Eckbo%20web%20site/AFA611-S6B-FamaFrench-CAPM-JEP04.pdf

Bessembinder, H. Do Stocks Outperform Treasury Bills

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2900447

S&P Dow Jones Indices

https://www.spglobal.com/spdji/

1 Diversification does not guarantee a profit nor protect against loss in any market.

Important Disclosure:

This material is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The views expressed are those of the author as of the date indicated and are subject to change without notice.

Forward-looking statements, including expectations regarding diversification, volatility, correlation behavior, portfolio construction, and market regimes, are inherently uncertain and are not guarantees of future results. There can be no assurance that any investment strategy or portfolio construction approach will achieve its objectives or perform as expected.

References to Modern Portfolio Theory, diversification, index construction, correlations, volatility, or historical market behavior are for illustrative purposes only and should not be interpreted as predictive of future market outcomes. Historical relationships among asset classes and securities may change over time and may not repeat in the future.

Investors should carefully consider their investment objectives, risks, charges, and expenses and consult their financial, legal, and tax advisors before making investment decisions.

Important Information

© 2026. Easterly Asset Management. All rights reserved.

As of March 31, 2026, Easterly Asset Management and its Strategic Partners had nearly $3.1B in managed assets which includes over $2.7B in assets under management and administration of Easterly Investment Partners LLC, an SEC registered investment adviser. Easterly Snow and Easterly Ranger are investment teams of Easterly Investment Partners LLC. EAB Investment Group LLC (d/b/a Easterly EAB) and Orange Investment Advisors LLC (d/b/a Easterly Orange) are separate SEC-registered investment advisers that are strategic partners of Easterly. Each investment adviser’s Form ADV is available at www.sec.gov. Registration does not imply and should not be interpreted to imply any particular level of skill or expertise.

No funds or investment services described herein are offered or will be sold in any jurisdiction in which such an offer or sale would be unlawful under the laws of such jurisdiction. No such fund or service is offered or will be sold in any jurisdiction in which registration, licensing, qualification, filing or notification would be required unless such registration, license, qualification, filing, or notification has been effected.

The material contains information regarding the investment approach described herein and is not a complete description of the investment objectives, risks, policies, guidelines or portfolio management and research that supports this investment approach. Any decision to engage the Firm should be based upon a review of the terms of the prospectus, offering documents or investment management agreement, as applicable, and the specific investment objectives, policies and guidelines that apply under the terms of such agreement. There is no guarantee investment objectives will be met. The investment process may change over time. The characteristics set forth are intended as a general illustration of some of the criteria the strategy team considers in selecting securities for client portfolios. Client portfolios are managed according to mutually agreed upon investment guidelines. No investment strategy or risk management techniques can guarantee returns or eliminate risk in any market environment. All information in this communication has been obtained from sources believed to be reliable but cannot be guaranteed. Investment products are not FDIC insured and may lose value.

Investments are subject to market risk, including the loss of principal. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate. The information contained herein does not consider any investor’s investment objectives, particular needs, or financial situation and the investment strategies described may not be suitable for all investors. Individual investment decisions should be discussed with a personal financial advisor.

Any opinions, projections and estimates constitute the judgment of the portfolio managers as of the date of this material, may not align with the Firm’s opinion or trading strategies, and may differ from other research analysts’ opinions and investment outlook. The information herein is subject to change without notice and may be superseded by subsequent market events or for other reasons. Easterly assumes no obligation to update the information herein.

References to securities, transactions or holdings should not be considered a recommendation to purchase or sell a particular security and there is no assurance that, as of the date of publication, the securities remain in the portfolio. Additionally, it is noted that the securities or transactions referenced do not represent all of the securities purchased, sold or recommended during the period referenced and there is no guarantee as to the future profitability of the securities identified and discussed herein. As a reminder, investment return and principal value will fluctuate.

The indices cited are, generally, widely accepted benchmarks for investment performance within their relevant regions, sectors or asset classes, and represent non managed investment portfolio. It is not possible to invest directly in an index.

This communication may contain forward-looking statements, which reflect the views of Easterly and/or its affiliates. These forward-looking statements can be identified by reference to words such as “believe”, “expect”, “potential”, “continue”, “may”, “will”, “should”, “seek”, “approximately”, “predict”, “intend”, “plan”, “estimate”, “anticipate” or other comparable words. These forward-looking statements or other predications or assumptions are subject to various risks, uncertainties, and assumptions. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. Should any assumptions underlying the forward-looking statements contained herein prove to be incorrect, the actual outcome or results may differ materially from outcomes or results projected in these statements. Easterly does not undertake any obligation to update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by applicable law or regulation.

Past performance is not indicative of future results.

20260623_5630989